What Is Activity Based Costing / Guide to what is activity based costing (abc) & its definition.

What Is Activity Based Costing / Guide to what is activity based costing (abc) & its definition.. Activity based costing is a costing method that has been developed to deal with the perceived the terms 'activity' and 'cost pool' are often used interchangeably. Identify what activity drives each cost. Simply, activity based costing overcomes the issue of assigning costs by machine hours by assigning overhead costs more logically through. Identify cost drivers for each activity, i.e. Costs are assigned to specific activities—planning, engineering, or manufacturing—and then the activities are associated with different products or services.

Identify cost drivers for each activity, i.e. Traditionally, in a job order cost system and process cost system, overhead is allocated to a job or function based on activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs. Definition by cima, cost attribution to cost units on the basis of benefit received from indirect activities e.g. Applying overhead costs to each product or service based on the extent to which that product or service causes overhead cost to be incurred is the primary objective of accounting for overhead costs. Activity based costing data will have to be linked to the evaluation of employees if you are looking to implement the system successfully.

What Is Activity Based Costing Abc Definition Meaning Example from myaccountingcourse.com Activity based costing first assigns costs to the activities that are the real cause of the overhead. Activity based costing is an accounting methodology used for assigning accurately the extent of resources consumed and overhead costs incurred definition of activity based costing. Benefits of using abc costing. Activity based costing approach for costing a product is known as a rational approach compared to the traditional overhead allocation, where overheads are allocated based on direct labour hour or machine hour consumption. Guide to what is activity based costing (abc) & its definition. In order to implement the abc method, you will need to do things like interview employees to decide which items will go in. Traditional costing is much easier to implement, whereas the abc method requires a lot of extra work. Definition by cima, cost attribution to cost units on the basis of benefit received from indirect activities e.g.

For example, one activity could be step 2:

Split fixed overheads into activities. What is activity based costing (abc)? Activity based costing is being introduced to solve the costing problems associated with the traditional costing method. Activity based costing approach determines the cost of a product based on the activities performed during its production. Activity based costing data will have to be linked to the evaluation of employees if you are looking to implement the system successfully. Activity based costing is a method used to allocate the overheads according to the level of activity. Next, let's see what impact these different allocation techniques and overhead rates would have on why is the cost of setting up a production machine so expensive? It divides the overheads into different cost pools and then allocates them. We can encounter that the benefits definitely overcome the disadvantages and therefore this system is worth for every. Abc costing focuses on identifying activities, or production processes, that are used to process a job. Is activity based costing applicable in today's modern economy and organizations? Next, you'll want to get a bit narrower with how you sort these costs by determining the cost drivers. Costs are assigned to specific activities—planning, engineering, or manufacturing—and then the activities are associated with different products or services.

Besides measuring the performance of an activity, this cost accounting technique helps to identify all the costs related to every unique activity. What an activity based costing example actually explains. Traditionally, in a job order cost system and process cost system, overhead is allocated to a job or function based on activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs. Guide to what is activity based costing (abc) & its definition. The first sometimes we may want to reduce the price to fight for market share, but we not sure what is the minimum amount.

Activity Based Costing Abc Definition Steps And Diagram from www.loscostos.info Activity based costing is being introduced to solve the costing problems associated with the traditional costing method. It identifies the activities in the organization such as the purchase of material is an activity of purchase. Activity based costing is a method used to allocate the overheads according to the level of activity. Activity based costing (abc) is a costing system that goes beyond traditional cost price models with respect to indirect cost calculation models. Besides measuring the performance of an activity, this cost accounting technique helps to identify all the costs related to every unique activity. For example, one activity could be step 2: It is defined as a costing method to identify activities in an organization and assign indirect and overhead costs. Simply, activity based costing overcomes the issue of assigning costs by machine hours by assigning overhead costs more logically through.

Traditionally, in a job order cost system and process cost system, overhead is allocated to a job or function based on activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs.

Activity based costing data will have to be linked to the evaluation of employees if you are looking to implement the system successfully. We have understood what activity based costing is and also understood its benefits and disadvantages. The abc process is as follows: Benefits of using abc costing. Activity based costing is a costing method that has been developed to deal with the perceived the terms 'activity' and 'cost pool' are often used interchangeably. What can be done to reduce the. Activity based costing approach determines the cost of a product based on the activities performed during its production. The abc formula can be explained with the following core concepts. Split fixed overheads into activities. Traditional costing is much easier to implement, whereas the abc method requires a lot of extra work. Next, let's see what impact these different allocation techniques and overhead rates would have on why is the cost of setting up a production machine so expensive? What causes these activity costs to be incurred. Is activity based costing applicable in today's modern economy and organizations?

It identifies the activities in the organization such as the purchase of material is an activity of purchase. Traditional costing is much easier to implement, whereas the abc method requires a lot of extra work. What an activity based costing example actually explains. Activity based costing (abc) is a costing system that goes beyond traditional cost price models with respect to indirect cost calculation models. Activity based costing first assigns costs to the activities that are the real cause of the overhead.

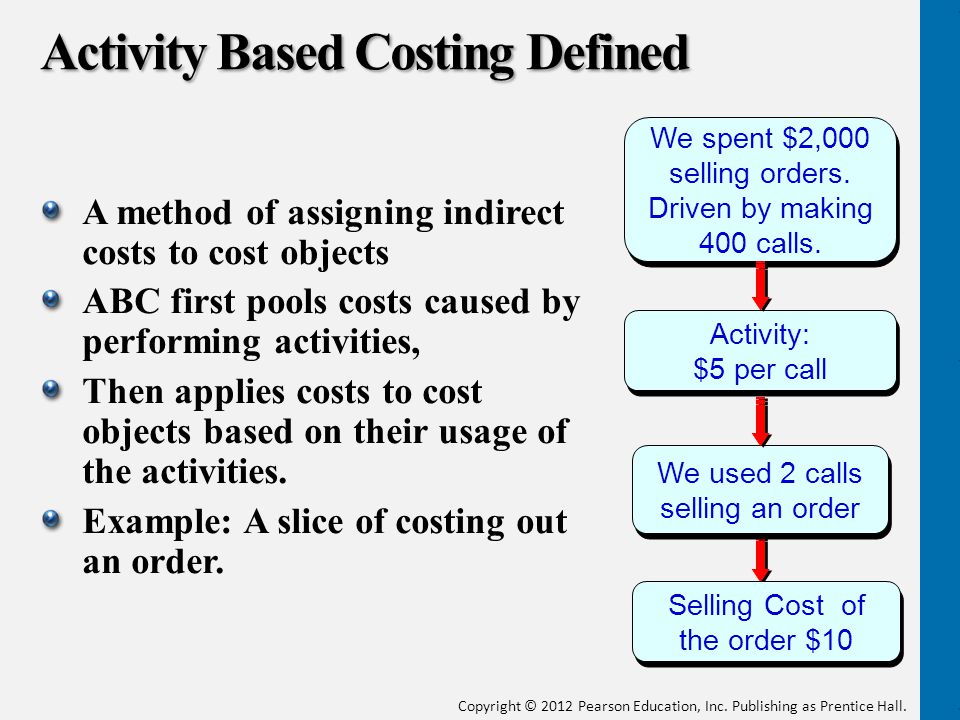

Activity Based Costing And Other Cost Management Tools Ppt Download from slideplayer.com Is activity based costing applicable in today's modern economy and organizations? The first sometimes we may want to reduce the price to fight for market share, but we not sure what is the minimum amount. Next, you'll want to get a bit narrower with how you sort these costs by determining the cost drivers. We have understood what activity based costing is and also understood its benefits and disadvantages. What is activity based costing (abc)? Traditionally, in a job order cost system and process cost system, overhead is allocated to a job or function based on activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs. Guide to what is activity based costing (abc) & its definition. Simply, activity based costing overcomes the issue of assigning costs by machine hours by assigning overhead costs more logically through.

Activity based costing is a costing method that has been developed to deal with the perceived the terms 'activity' and 'cost pool' are often used interchangeably.

Benefits of using abc costing. Activity based costing is typically seen in various small businesses, especially in manufacturing. Split fixed overheads into activities. For example, one activity could be step 2: In order to implement the abc method, you will need to do things like interview employees to decide which items will go in. In many production processes, overhead is applied to. Costs are assigned to specific activities—planning, engineering, or manufacturing—and then the activities are associated with different products or services. Traditionally, in a job order cost system and process cost system, overhead is allocated to a job or function based on activity‐based costing assumes that the steps or activities that must be followed to manufacture a product are what determine the overhead costs. Abc costing focuses on identifying activities, or production processes, that are used to process a job. The first sometimes we may want to reduce the price to fight for market share, but we not sure what is the minimum amount. Activity based costing is a costing method that has been developed to deal with the perceived the terms 'activity' and 'cost pool' are often used interchangeably. Identify the process and cost pool: Activity based costing data will have to be linked to the evaluation of employees if you are looking to implement the system successfully.

Related : What Is Activity Based Costing / Guide to what is activity based costing (abc) & its definition..